Gulf states spend big to buffer coronavirus crisis

Gulf states spend big to buffer coronavirus crisis

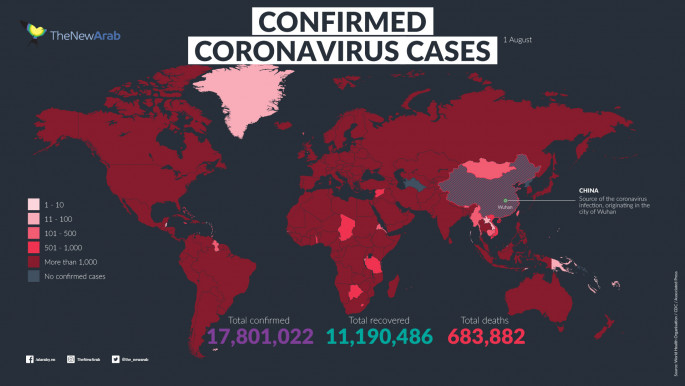

The coronavirus pandemic looks set to cost the Gulf states billions, just as the region looks to move into a post-oil future.

6 min read

Thousands of residents have been locked out of Gulf countries [Getty]

Governments across the world are responding to the economic impact caused by the coronavirus crisis with extensive bailout packages on a scale not seen for decades.

The Gulf region is no exception, hit hard by a huge drop in oil prices, a freeze on tourism, and the near decimation of parts of the service sector.

Yet the enormous wealth and financial reserves of the Gulf states will help cushion the blow, with radical steps taken to contain the spread of the virus, although the crisis comes at a critical juncture.

Saudi Arabia, the UAE, Oman and other Gulf countries have been reliant on oil reserves for decades, but have taken more serious steps to shrink the state and create more diverse economies.

Dubai's Expo 2020 is one example, an event the UAE has been anticipating for almost a decade - dubbed "the Greatest Show on Earth" - and expected to propel the country into a new era. It is threatened to be put on hold due to the coronavirus outbreak.

The coming decade was expected to see an explosion in the SME sector but the financial crisis will mean many businesses will have to rely on state bailouts to survive the coming months.

Twitter Post

|

Airlines look set to be hit hard, with aircraft grounded and travel restrictions and once-bustling airports left empty.

Although some hotels have been reconditioned as quarantine centres, the vast majority remain dormant.

Here is how the Gulf states are dealing with the crisis:

Qatar

Cases: 460 cases, 0 deaths (20/3/2020)

Travel restrictions: Non-Qataris barred from entry

Public restrictions: Most public places closed

The global pandemic has seen Doha take tough measures to prevent a major outbreak of the coronavirus but a financial impact on business has been inevitable.

To help businesses weather the storm, the Supreme Committee for Crisis Management - set-up to deal with the coronavirus outbreak – has announced a 75 billion riyal ($20 billion) stimulus package.

This includes exempting tourism, retail and logistics businesses from water and electricity bills for the next six months, and other tax breaks.

Banks have also been instructed to put any loan repayments from businesses on hold for the next six months. The government will also pump 10 billion riyals ($2.7 billion) into capital markets to boost the economy.

|

The enormous wealth and financial reserves of the Gulf states will help cushion the blow, with radical steps taken to contain the spread of the virus |  |

UAE

|

|

| Click to enlarge |

Cases: 140 cases, 0 deaths (20/3/2020)

Travel restrictions: Non-Emiratis barred from entry

Public restrictions: Most public places closed

The UAE government has also offered a huge stimulus package to deal with the battering from a huge drop in oil prices and downturn in tourism.

The 15-point plan, named Ghadan 21, is focused mainly on easing loan burdens for small businesses, as well as cutting bills and taxes.

The UAE Central Bank said it would pump 100 billion dirhams ($27 billion) into the economy, half from the bank's own funds and the other 50 billion dirhams through capital buffers from other banks.

Businesses and other clients can also avail of temporary relief from loan payments over the next six months.

A bail-out package has also been unveiled for struggling SMEs, including 3 billion dirhams ($816,771) for loans for SMEs and a cancelling of a range of fees. Subsidies are also being increased for citizens and businesses.

Saudi Arabia

Cases: 274 cases, 0 deaths (20/3/2020)

Travel restrictions: Tourist visas and all flights suspended

Public restrictions: Most public places closed

Saudi Arabia's gamble on boosting oil production has seen the price of a barrel crash below the $30 mark, leading to panic in the kingdom.

Saudi Aramco's shares have fallen 18 percent with the company's value dropped from $2 trillion to $1.5 trillion - another big blow for Crown Prince Mohammed bin Salman's Vision 2030 diversification plans.

Hopes for revolutionary growth in non-oil sectors will also be severely dented by the huge impact the virus has had on businesses, particularly in the tourism and leisure sectors.

The government said it will introduce new fiscal measures to dampen the blow for Saudi businesses and banks, although the scope of the stimulus - so far - appears to be much smaller than some other Gulf states.

The Saudi Monetary Authority is looking at a 50 billion riyals ($13 billion) bail-out plan, particularly aimed at helping small and medium size businesses affected by the crisis - mostly aimed at easing their debt burden for the next six months.

|

|

Bahrain

Cases: 284 cases, 1 death (19/3/2020)

Travel restrictions: Visas-on-arrival suspended, compulsory self-isolation for two weeks

Public restrictions: Schools closed, limited opening hours at some malls

Bahrain has been one of the hardest hit Arab Gulf states by the coronavirus pandemic, recording the first death from the disease in the GCC region.

Manama is not just dealing with an unprecedented public health crisis but, with dwindling oil supplies, an economic one.

Bahrain's tourism and service sectors will be the hardest hit by the crisis, with flights to neighbouring Saudi Arabia grounded and the coveted Grand Prix race postponed.

The response from the government has been significant, with a bail-out package valued at almost a third of the island state's GDP set to be unrolled. If passed, the eight-point $11 billion package could see private sector workers' wages being covered for three months, as well as water, utility bills being paid by the state for a similar period.

Loans will be also issued to smaller businesses and debt repayments put on hold to help with liquidity in the market. On Thursday, Reuters revealed that Bahrain was looking to raise $1 billion in funds through loans from banks.

|

Saudi Arabia, the UAE, Oman and other Gulf countries have been reliant on oil reserves for decades, but have taken more serious steps to shrink the state and create more diverse economies | |

Oman

Cases: 48 cases, 0 deaths (19/3/2020)

Travel restrictions: Non-Omanis - except GCC citizens - barred, tourists told to leave

Public restrictions: Most public places closed

The sultanate's tourism drive has been hurt over the coronavirus crisis, with entry barred to foreigners and a temporary freeze on visas.

Earlier in the week, the ministry of finance made five percent cuts to the budgets of government departments due to debt burdens and low oil prices, according to Reuters.

By the end of the week, Oman announced a huge 8 billion rials ($20 billion) stimulus package to battle the economic impact of the coronavirus crisis and cuts to interest rates should encourage borrowng and spur growth.

The scheme appears aimed chiefly at allowing banks to offer more loans to businesses and defer payments to ease the pressure on the private sector.

Restaurants and commercial enterprises will be exempt from municipality taxes until the end of August and factories will pay no rent for the next three months.

To ensure vital supplies still enter the country, Oman is reducing costs for importers, increasing food stocks and opening up government warehouses for the private sector free-of-charge.

Kuwait

Cases: 159 cases, 0 deaths (19/3/2020)

Travel restrictions: Non-Kuwaitis barred from entry

Public restrictions: Partial lockdown

Kuwait has implemented a partial lockdown of the capital, with public life put on hold.

Kuwait's private sector will likely be battered by the slowdown in economic activity and low oil prices with the government's deficit set to widen.

With the country's reliance on oil for income and the huge numbers of Kuwaitis working in the private sector is perhaps factors in why the government has been slow to respond with no bail-out packages unveiled yet.

Follow us on Facebook, Twitter and Instagram to stay connected

![Minnesota Tim Walz is working to court Muslim voters. [Getty]](/sites/default/files/styles/image_684x385/public/2169747529.jpeg?h=a5f2f23a&itok=b63Wif2V)